每周全球金融观察 | 第 149 篇:美国评级从 AAA 下调至 AA+:噪音还是实质?

来源:岭南论坛 时间:2023-08-07

8 月 1 日(收市后),惠誉评级公司将美国评级从 AAA 下调至 AA+。惠誉是美国三家评级机构之一,另外两家是穆迪和标准普尔(又称标普)。8 月 2 日,道指、标普 500 指数和纳斯达克指数分别下跌了 0.98%、1.38% 和 2.17%。10 年期 UST 的收益率上升了 6 个基点(如果从 7 月 31 日算起,则为 12 个基点)。

惠誉和穆迪之前对美国的评级为 AAA,标准普尔为 AA+。现在,标准普尔和惠誉的评级为 AA+,穆迪的评级为 AAA。惠誉的评级下调是噪音还是实质?

许多人可能还记得,标普在 2011 年 8 月 5 日星期五(收市后)下调了美国的评级。周一(2022 年 8 月 8 日),道指、标普 500 指数和纳斯达克指数分别下跌了 5.55%、6.66% 和6.90%。与市场预期相反,10 年期美国国债出人意料地反弹,当日收益率降低了 24 个基点。这让人们意识到,美国是全球最强大的经济体。即使标普下调评级,您更愿意持有哪种主权债券?

与 2011 年 8 月 8 日(星期一)相比,2023 年 8 月 2 日(星期三)的反应是 "缄默 "的。周三华尔街交易员之间的笑话是:"贞操不能丢两次" 。

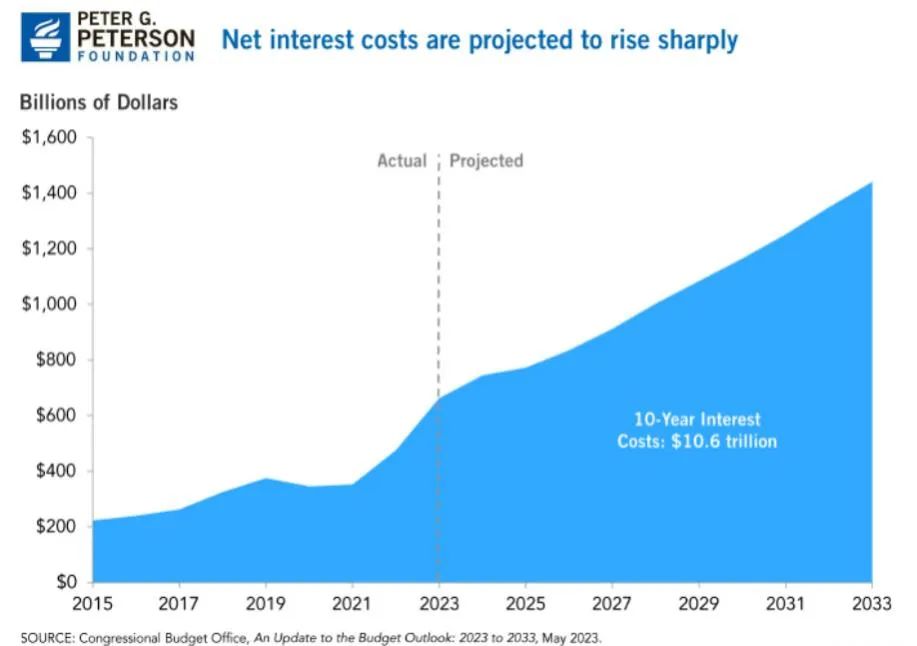

降级提醒我们,美国需要认真对待财政责任。债务降级还不是一个严重的问题,但它是一个信号,表明金融市场对政府认真对待债务的意愿的信心正在下降。美国国会预算办公室(CBO)预计,2023 财年的利息支出总额将达到 6630 亿美元,并在未来十年内迅速上升--从 2024 年的 7450 亿美元攀升至 2033 年的 1.4 万亿美元。总之,未来十年的净利息支出总额将接近 10.6 万亿美元。相对于经济规模,利息将从 2024 财年占 GDP 的 2.7% 上升到2033 财年的 3.7%。

更重要的是如果标普和惠誉同时下调美国评级,那将是灾难性的。相隔 12 年的差别可谓天壤之别。2011 年,当标普下调美国评级时,人们感到震惊和担忧,因为许多金融合同都规定抵押品必须达到 "AAA "级。由于美国的评级被拆分,仍为 AAA 级(2 对 1),因此躲过一劫。

在随后的 12 年里,大多数金融合同都被改写为包含 "美国政府支持的债务 "或类似的字眼。因此,这不会导致回购、贷款、衍生品(如期货交易所的保证金)和投资合同(如 "政府"共同基金和货币市场基金)的强制平仓。

2011 年全年,道琼斯指数、标准普尔指数和纳斯达克指数的回报率分别为 +5.52%、0.00% 和 -1.80%。降级后(2011 年 5 月 8 日至 2011 年 12 月 30 日)的收益率分别为 +6.75%、+4.86% 和 +2.87%。2011 年末,10 年期 UST 收益率下降了 142 个基点(2011 年 12 月 30 日为 1.877%,2010 年 12 月 31 日为 3.295%),降级后 5 个月的收益率为 1.877%,2011 年 8 月 5 日为 2.560%。)

道琼斯指数、标准普尔 500 指数、纳斯达克指数:2011 - 2014 年回报率

我的拙见是,惠誉在 8 月 1 日的降级只是一个噪音。它对美国经济或股市的影响为零。

无论美国的评级是 AAA 还是 AA+,都不会影响最新的人工智能创新,也不会影响已经渗透到我们日常工作和生活方方面面的互联网应用。这也不会影响消费者的消费。

巧合的是,本周美国和全球股市都出现了抛售,这也是我们在进入历史上股市回报率最差的月份(9 月/10 月)之前获利了结的一个借口。我相信,尽管未来几个月可能会崎岖不平,但牛市仍将继续,道琼斯指数、标准普尔指数和纳斯达克指数很有可能在 12 月 31 日高于目前的水平。

不过,我对长期利率(10 年期 UST)不那么乐观。2011 年的奇迹不会在 2023 年重演。本周,所有主要固定收益指数均收红。长期利率走高将是主旋律。

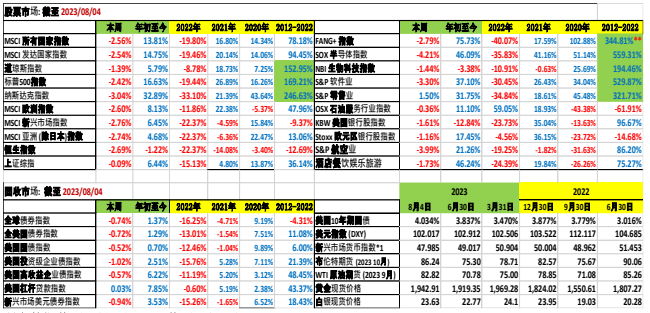

请参阅下表,了解 2023 财年与往年的业绩对比:

所有数据截至 8 月 4 日,*1 截至 8 月 3 日

我们将何去何从?

全球股票市场:

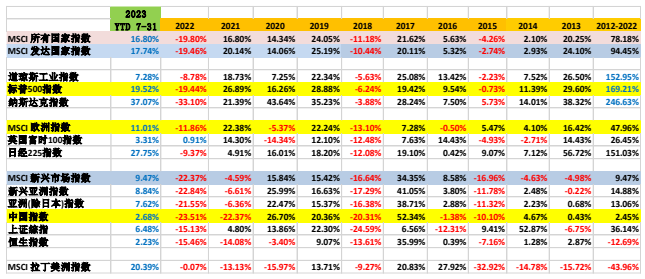

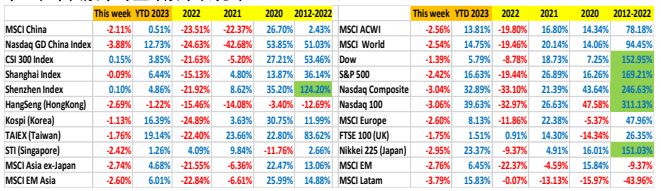

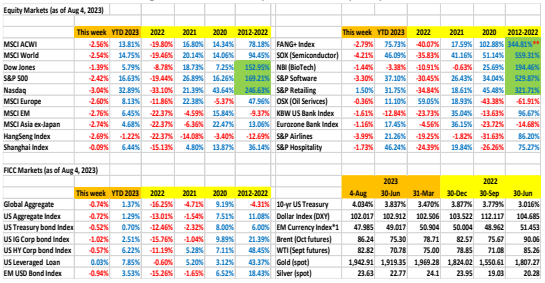

全球主要股票指数在 7 月份均以高位收盘。道指、标普 500 指数和纳斯达克指数当月分别上涨 3.35%、3.11% 和 4.05%,7 月 31 日至今分别上涨 7.28%、19.52% 和 37.07%。MSCI欧洲指数(MSCI Europe)和日经 225 指数今年以来分别上涨 11.01% 和 27.75%。新兴市场股票在 7 月份表现抢眼。MSCI 中国和恒生指数本月分别上涨 9.30% 和 6.15%,年初至今转为正值。MSCI 拉丁美洲指数在 7 月份上涨了 5%,年初至今的涨幅更是高达 20.39%。

7 月份和年初至今全球股市表现优异的主要原因是:a) 通胀回落;b) 加息周期预期结束;c) 全球经济(尤其是美国)出人意料地恢复了活力。

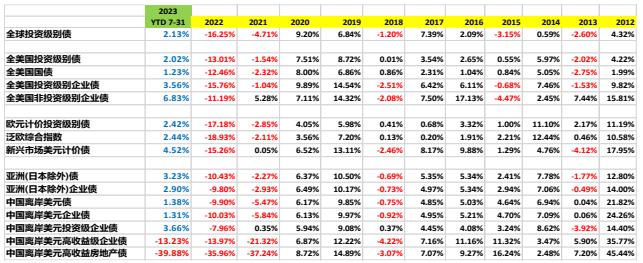

全球固定收益市场:

与全球股市相比,全球固定收益市场的表现并不突出,回报率仅为个位数。距离降息还有几个月的时间,固定收益市场将不得不面对几个月的逆风,以及延迟降息带来的暴利。

最令人期待的经济衰退终究不会到来:

上周加息后,美国联邦储备委员会主席鲍威尔周三表示,央行工作人员不再预测美国经济衰退,"我们确实有机会 "在不出现高水平失业的情况下让通胀率回归目标。许多私营部门的经济学家最近也加入了这一行列。

周五公布的 7 月份非农就业报告显示,7 月份新增就业岗位 18.7 万个,而预测值为 20 万个(6 月份为+18.5 万个),这几乎是劳动力市场的 "天时地利 "环境。

亚特兰大联储的实时 GDPNow 模型预计第三季度国内生产总值将增长 3.9%。

CBO 对未来 10 年美国利息支出的预测(见第一页底部的图表)可能会降低您锁定未来 10 年收益率为 4.03% 的 10 年期美国国债的热情。

做好 "长期走高 "的准备。我指的是利率。

作者:蔡清福

Alvin C. Chua

2023 年 8 月 5 日, 星期六

东亚和中国股票市场的表现与全球同行的比较:

Article #149:USA rating from AAA to AA+: Noise or substance?

On August 1 (after the market closed), Fitch Ratings Inc. downgraded USA rating to AA+ from AAA. Fitch is one of three rating agencies in America, the other two being Moody’s and Standard and Poor’s (aka S&P). On August 2, Dow, S&P500, and Nasdaq declined 0.98%, 1.38% and 2.17% respectively. The yield on the 10-year UST was higher by 6bp (12bp if counting from July 31).

USA was split rated with Fitch and Moody’s at AAA and S&P at AA+. Now it is S&P and Fitch at AA+ and just Moody’s with AAA. Is the Fitch rating downgrade noise or substance?

Many of us would remember that S&P downgraded USA rating on Friday August 5, 2011 (after the market closed). On Monday (Aug 8, 2011) the Dow, S&P500 and Nasdaq declined 5.55%, 6.66% and 6.90% respectively. Contrary to market expectations, the 10-year UST bond surprisingly rallied, with yield lowered by 24bp on that day. It drove home the fact that USA is the strongest economy on the planet. Even with the S&P downgrade, which sovereign bond would you rather own?

Compared to Monday August 8, 2011, the reaction on Wednesday August 2, 2023 was MUTED. The joke among Wall Street traders on Wednesday was: “you can’t lose your virginity twice”.

The downgrade is a reminder that USA needs to take fiscal responsibility seriously. The downgrading of the debt is not yet a serious problem, but it is a signal that financial market confidence in the government’s willingness to take debt seriously is declining. The Congressional Budget Office (CBO) projects that interest payments will total $663 billion in fiscal year 2023 and rise rapidly throughout the next decade — climbing from $745 billion in 2024 to $1.4 trillion in 2033. In total, net interest payments will total nearly $10.6 trillion over the next decade. Relative to the size of the economy, interest will rise from 2.7 percent of GDP in fiscal year 2024 to 3.7 percent in 2033.

It would have been catastrophic if S&P and Fitch were to concurrently downgrade USA rating. 12 years apart made a world of difference. When S&P downgraded the US in 2011, it was a shock and concern as many financial contracts were written that collateral had to be "AAA" rated. Since the US was split-rated and still AAA (2 vs 1), it dodged the bullet.

In the subsequent 12 years, most of these financial contracts have been rewritten to include "debt backed by the US Government" or words to this effect. So, this will NOT lead to a forced unwind of repos, loans, derivatives (like margin at futures exchanges), and investment contracts (like "Government" mutual funds and money market funds).

For the full year 2011, the Dow, S&P, and Nasdaq returned +5.52%, 0.00%, and -1.80%respectively. Counting post downgrade (8/5/2011-12/30/2011) were +6.75%, +4.86%, and+2.87%. The yield for the 10-year UST ended the year 2011 142bp lower (1.877% on 12/30/2011 vs 3.295% on 12/31/2010), counting the 5-months after the downgrade was 1.877% vs 2.560% on Aug 5, 2011).

It is my humble opinion that the Fitch downgrade on Aug 1 was NOISE. It will have zero effect on the US economy or the equity markets.

Whether USA rating is AAA or AA+ will have zero impact on the latest AI innovations, nor the internet applications that have permeated to every aspect of our everyday work and life. It will have no impact on consumer spending.

The US and global equity markets sold off this week, coincidentally, or an excuse to take some profits before we enter the historically worst months (Sept/ Oct) for stock market returns. I believe the bull market will continue, despite the likelihood of bumpy months ahead, with high probability that Dow, S&P and Nasdaq will be higher on Dec 31 than current levels.

However, I am less sanguine on long-term interest rates (10-yr UST). The miracle of 2011 will NOT repeat in 2023. All major fixed income indices were in the red this week. Higher for longer will be the dominant theme.

All data as of August 4, *1 as of August 3

Every major global equity index closed out the month of July on a high note. The Dow, S&P 500, and Nasdaq gained 3.35%, 3.11% and 4.05% for the month, and 7.28%, 19.52% and 37.07% gains YTD July 31. MSCI Europe and Nikkei 225 gained 11.01% and 27.75% YTD. EM equities were the star performer in July. MSCI China and HangSeng Index gained 9.30% and 6.15% for the month, and turn positive YTD. MSCI Latam gained 5% in the month of July, and an impressive 20.39% YTD.

The month of July and YTD global equity market outperformance was primarily driven by a) receding inflation, b) end of rate hike cycle expectation, and c) surprising resilience in global economies, especially in the US.

The global fixed income markets were less illustrious compared to global equities, with low single digit returns YTD July. With rate cuts likely to be months away, the fixed income markets will have to contend with months of headwind, and the delayed rate cut windfall.

After the rate hike last week, U.S. Fed Chairman Powell said on Wednesday that the central bank's staff no longer forecasts a U.S. recession, and "we do have a shot" for inflation to return to target without high levels of job losses.” Many private sectors economists have recentlyjumped on the same bandwagon.

Friday’s July payroll report with 187,000 jobs added in July vs a forecast of 200,000 (and +185,000 in June) was almost a goldilocks environment for the labor market.

The Atlanta Fed’s real time GDPNow model is projecting 3.9% GDP growth for Q3.

The CBO forecast on US interest payments for the next 10 years (see graph at the bottom of page one) may diminish your enthusiasm to lock in 10-year US Treasury bond at 4.03% yield for the next 10-years.

Be prepared for “Higher for Longer”. I meant interest rates.