每周全球金融观察 | 第138篇:我们可以把银行业的系统性风险排除掉

来源:岭南论坛 时间:2023-03-31

上周末,两项巨大的政策行动拯救了硅谷银行的储户,并使人们担心的银行业系统性风险得以平息。首先,FDIC为SVB的所有储户(25万美元以上)提供了担保。第二,美联储制定了银行定期融资计划(BTFP),银行可以按面值向美联储提交合格的抵押品(美国国债、美国政府机构债券和美国政府机构MBS)做抵押融资,而不管市场价格如何。这意味着银行可以按面值向美联储抵押贷款,而不管市值是多少。如果BTFP计划在一周前就已经实施,那SVB就不会破产了。

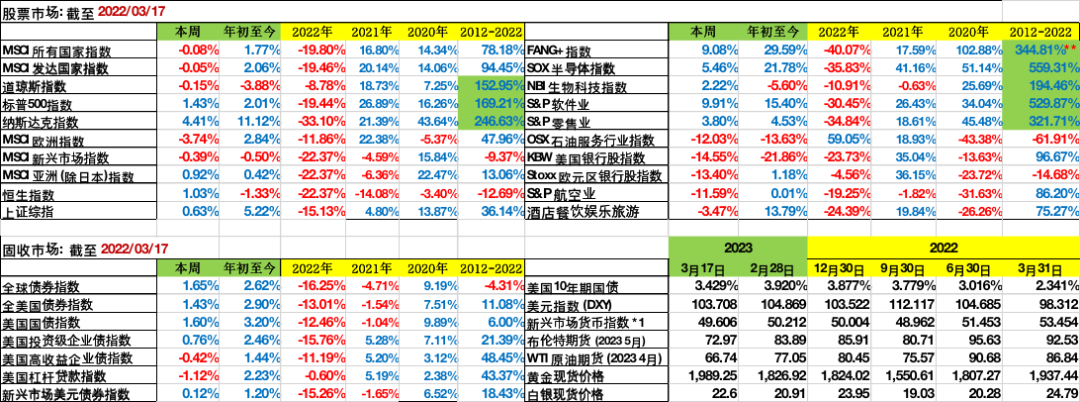

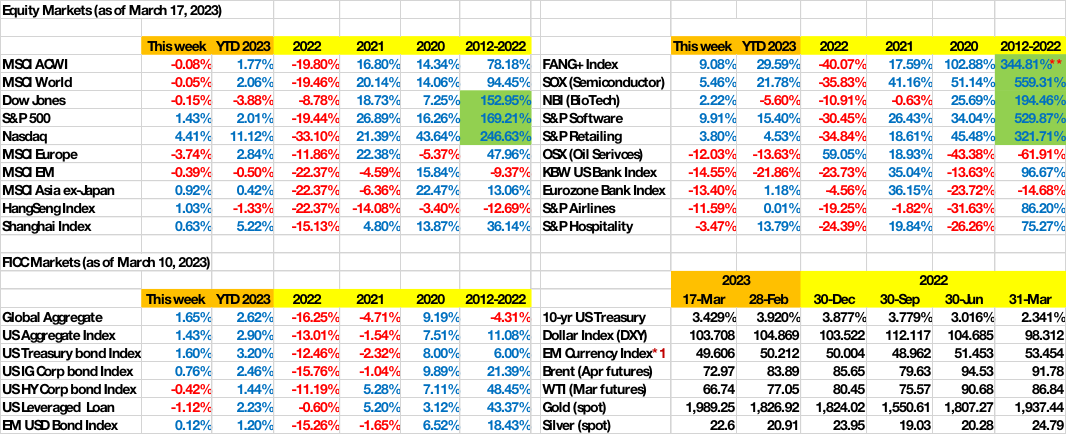

周四又有一个好消息传来。在财政部长珍妮特-耶伦和摩根大通董事长兼首席执行官杰米-戴蒙的策划下,11家银行组成的财团向第一共和银行注入了300亿美元的存款。在SVB和Signature Bank失败后,现金注入代表了一种私人市场解决方案,以阻止第一共和银行转瞬即逝的储户,并将第一共和银行变成一道防火墙。这也让人想起1998年对长期资本管理公司的救援,当时有14家银行向LTCM注入了36亿美元,然后解除了其与华尔街各银行的超杠杆头寸和衍生品风险敞口,这可能会造成系统性的传染(注意,没有涉及纳税人的钱)。尽管如此,KBW(BKX)美国银行业指数本周下跌14.55%,全年下跌21.86%。SPDR标准普尔区域银行ETF(KRE)本周下跌14.30%,全年下跌26.05%。我们必须记住,客户存款的安全性并不能转化为银行股东的回报。

KBW(BKX)美国银行指数和标准普尔区域银行ETF(KRE)。YTD回报率(%)

上周末发生的事情实际上是美国银行系统盈利能力的国有化。展望未来,银行将需要为客户的存款支付更高的保险(有人需要支付FDIC的一揽子保险),对银行风险承担业务的监管也会越来越多。公用事业的市盈率与私营企业相比要低得多。

受人尊敬的联邦存款保险公司前主席、金融稳定中心高级研究员谢拉-贝尔在《金融时报》上撰文指出:"美国监管机构正在为硅谷银行开一个危险的先例。

https://www.ft.com/content/b860ebb6-f202-4ec6-a80c-8b1527c949f4

在大西洋彼岸,瑞士信贷银行很脆弱。周三,股票下跌超过30%,CDS超过1000,债券交易处于不良水平。然后,午夜传来好消息,SNB(瑞士国家银行)为瑞士信贷提供了50亿瑞士法郎的信贷额度。瑞士信贷的最坏情况(信用风险)可能已经过去,尽管该银行机构的未来还不确定。

2023年YTD的业绩与往年相比,请参考下表:

所有数据截止到3月17日,*1:截止到3月16日

我们该何去何从?

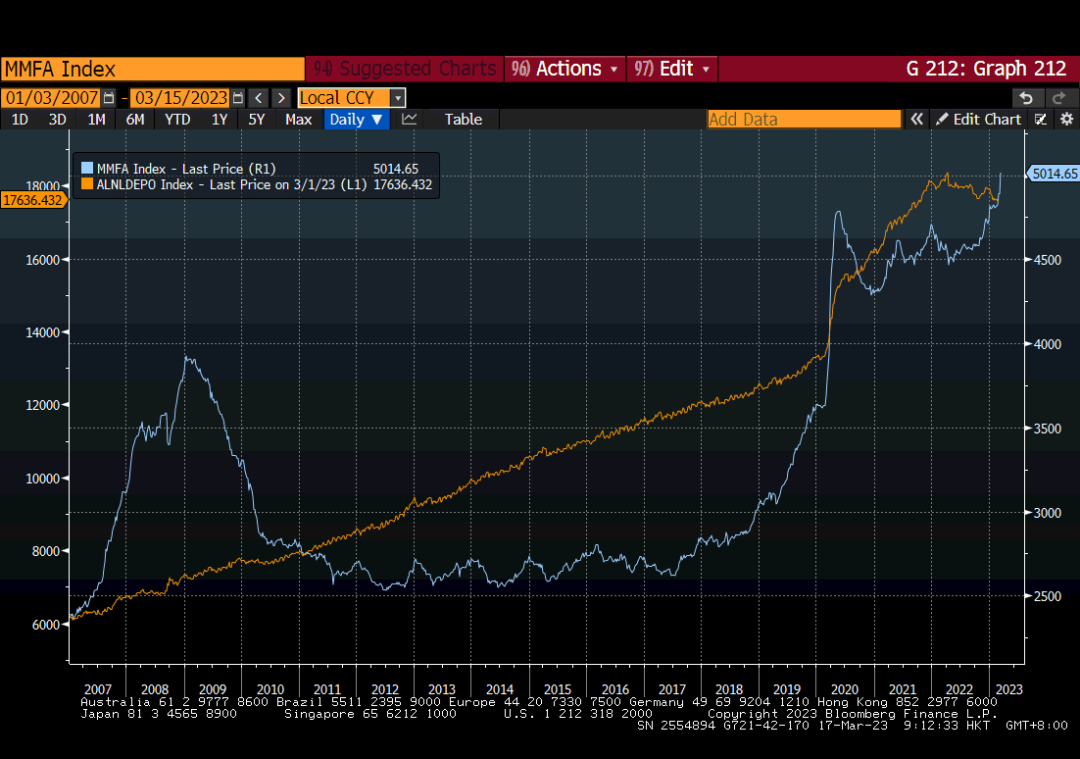

现金涌入美国货币市场基金

在银行业的动荡中,投资者在截至3月15日的一周内向货币市场基金注入了1200亿美元。货币市场基金资产达到了5万亿美元的历史新高。一个有效的问题是:当收益率开始下降时,这些堆积如山的货币市场基金资产会发生什么?我们可以把2009年作为一个先例吗?

美国货币市场基金资产(@3/15)和银行存款(@3/1)。

同样有趣的是,在将近一年的QT(QE逆转)之后,美联储的资产负债表在上周再次扩大。

欧洲央行周四继续按计划(上个月预先宣布)加息50个基点,将欧元区的基准利率从2.5%提高到3.0%。这是一个分裂的决定,3-4名管理委员会成员希望最快在本周停止加息,但尽管如此,大多数人还是保留了原计划,以显示对欧元区银行系统的信心。然而,欧洲央行放弃了保持"以稳定的步伐大幅提高利率 "的承诺。

即将召开的FOMC会议是下周三3月22日。美联储是按下暂停键还是继续进行最后的25个基点的加息?请继续关注....

衰退的概率已经增加

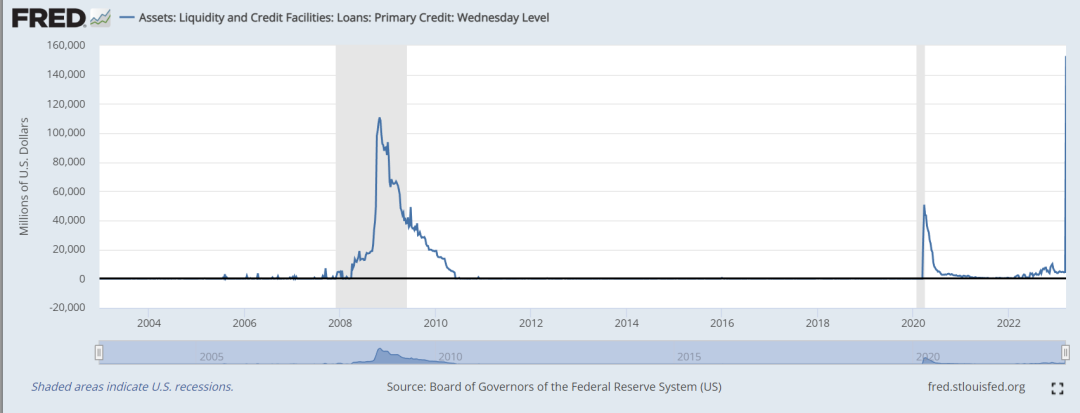

截至3月15日的一周,美联储初级信贷贴现窗口贷款已爆炸性增长至1529亿美元,明显高于2020年的经济衰退,也高于2008年的经济衰退。在1529亿美元中,只有119亿美元是新的BTFP。这是一个值得监测的数据点。

然而,银行业的动荡提高了美国经济衰退的概率。尽管银行业的系统性风险被FDIC对SVB储户的全面担保和美联储的BTFP所控制,但SVB的倒闭给科技生态系统带来的影响仍有待确定。转折点可能主要取决于私营部门的信心。

巧合的是,密歇根大学的消费者情绪指数四个月来首次下降,这并不是因为SVB,因为85%的调查是在SVB崩溃之前完成的。该指数的所有组成部分相对均匀地恶化,主要是由于持续的高价格,为情绪创造了下降的动力,最终导致上周SVB的消亡。这到底是狗被尾巴打,还是压垮虚弱骆驼的稻草?

2022年无情的加息已经抑制了房地产行业,并使整个股票和固定收益资产类别的投资者感到慌乱。所有以前的四次经济衰退(1990年、2001年、2008年和2020年)都是由打破虚弱的骆驼的冲击引发的(1990年:伊拉克入侵科威特,2001年:9/11恐怖袭击,2008年:雷曼的崩溃,2020年。Covid-19的爆发)。 我们必须向监管机构致敬,因为他们采取了迅速和果断的行动来控制银行业的后果。也许剩下的最后一个挽救经济衰退的办法是美联储暂缓进一步加息,先发制人地降息(并容忍高于平均水平的通货膨胀)。

利率市场的交易就像经济衰退迫在眉睫一样。2年期美国国债收益率从周三(3月8日)的5.07%下降到周五的3.84%(7个交易日内前所未有的121bp下降),同期10年期美国国债收益率从3.99%下降到3.43%。

美联储(和欧央行)面临艰难的选择:金融稳定还是通货膨胀。市场定价超越了对美联储由于金融稳定将眨眼。市场此时此刻押注了美联储将很快降息。请继续关注...

作者:蔡清福

Alvin Chua

2023年3月18日,星期六

东亚和中国股票市场的表现与全球同行相比

截至2023年3月17日的数据

Two dramatic policy actions last weekend rescued the depositors of Silicon Valley Bank, and put the much-feared banking systemic risk to rest. The first was the FDIC provided guarantee for all the SVB depositors (above US$250,000). The second was the Fed set-up the Bank Term Funding Program (BTFP) where-by banks can post eligible collaterals with the Fed (UST, Agency Securities, and Agency MBS) at face value, regardless of market price. What it means is banks can post under-water securities with Fed at PAR value, regardless of the market value. If the BTFP program has been in-placed a week ago, SVB would not have gone under.

There was another good news on Thursday. Orchestrated by Treasury Secretary Janet Yellen and JP Morgan Chairman & CEO Jamie Dimon, a consortium of eleven banks injected US$30 billion of deposits into First Republic Bank. The cash infusion represented a private market solution to stem First Republic’s fleeting depositors and turned First Republic into a firewall, after the failure of SVB and Signature Bank. It also reminisces the 1998 rescue of Long-Term Capital Management whereby fourteen banks injected $3.6bn into LTCM, then unwound its ultra-leveraged positions and derivative exposures with banks across Wall Street which threatened systemic contagion (note that no tax payer money was involved). Nevertheless, the KBW (BKX) US bank index was off 14.55% this week, and -21.86% YTD. The SPDR S&P Regional bank ETF (KRE) was off 14.30% and -26.05% YTD. We must remember, safety in customer deposit does not necessarily translate into equity shareholder return.

What effectively happened last weekend was the nationalization of the American banking system’s profitability. Going forward, banks will need to pay for higher insurance for customer deposits (someone will need to pay for the FDIC blanket insurance), and there will be increasing regulation of bank risk taking businesses. Public utility trades at much lower P/E multiples vs private enterprise.

Sheilla Bair, the well-respected former chair of FDIC and a senior fellow at the Center for Financial Stabilitypenned "US regulators are setting a dangerous precedent on Silicon Valley Bank" in the Financial Times:

https://www.ft.com/content/b860ebb6-f202-4ec6-a80c-8b1527c949f4

Across the Atlantic, Credit Suisse was vulnerable. On Wednesday, the stock was down over 30%, CDS was over 1000, and bonds were trading at distressed levels. Then came the mid-night good news that SNB (Swiss National Bank) provided a Sfr 50 billion credit line for Credit Suisse. The worst (credit risk) for Credit Suisse is likely over, although the future of the banking institution is uncertain.

All data as of March 17, *1: as of March 16

Amid the turmoil in the banking sector, investors poured US$120 billion into money market funds for the week ending March 15. MMF assets reached a new all-time high of US$5 trillion. A valid question to ask would be: what would happen to this mountain of MMF assets when yields start to decline? Could we use 2009 as a precedent?

It is also interesting to note that after almost a year of QT (QE reversal), the Fed balance sheet began to expand again last week.

The ECB went ahead with a planned (pre-announced last month) 50bp rate hike on Thursday, bringing the Eurozone benchmark rate from 2.5% to 3.0%. It was a split decision with 3-4 of the governing council members wanting to stop raising rate as soon as this week, but nevertheless, the majority kept the original plan to show confidence in the Eurozone banking system. However, ECB dropped the commitment to keep “raising interest rate significantly at a steady pace” wording.

Theupcoming FOMC meeting is next Wednesday March 22. Will the Fed hit the pause button or go ahead with a final 25bp rate hike? Stay tuned ….

The Fed primary credit discount window lending has exploded to US$152.9 billion for the week ending March 15, significantly higher than the 2020 recession and higher than the 2008 recession. Just $11.9 billion out of the $152.9 billion is the new BTFP. It is a data point worth monitoring.

Nevertheless, the turmoil in the banking sector has raised the odds of recession in the US. Despite the banking sector’s systemic risk being contained by the FDIC blanket guarantee of SVB depositors and the Fed BTFP, the fall-out in the tech eco-system resulting from the collapse of SVB is yet to be determined. The tipping point may depend largely on the private sector confidence.

Coincidentally, theUniversity of Michigan's index of consumer sentiment fell for the first time in four months, not because of SVB, since 85% of the surveys were done prior to the SVB collapse. All components of the index worsened relatively evenly, primarily due to persistently high prices, creating downward momentum for sentiment, culminating in last week’s SVB demise. Was it the tail that whacked the dog, or the straw that broke the weakened camel’s back?

The persistent interest rate hikes of 2022 have dampened the real-estate sector, and rattled investors across equity and fixed income asset classes. All the previous four recessions (1990, 2001, 2008 and 2020) were triggered by shocks that broke the weakened camel’s back (1990: Iraq’s invasion of Kuwait, 2001: 9/11 terrorist attack, 2008: the collapse of Lehman, 2020: Covid-19 break-out). We must salute the regulators for their swift and decisive actions to contain the banking fall-out. Perhaps the last remaining salvation from a recession is the Fed holding off on further rate hikes and pre-emptively cutting rates (and tolerating above average inflation).

The Fed (and ECB) has a Tough Choice: financial stability or inflation. The market is more than pricing-in that the Fed willblink as financial stability is at stake. Market at this juncture is betting that the Fed will be cutting interest rate soon. Stay tuned …

By Alvin Chua

Saturday March 18